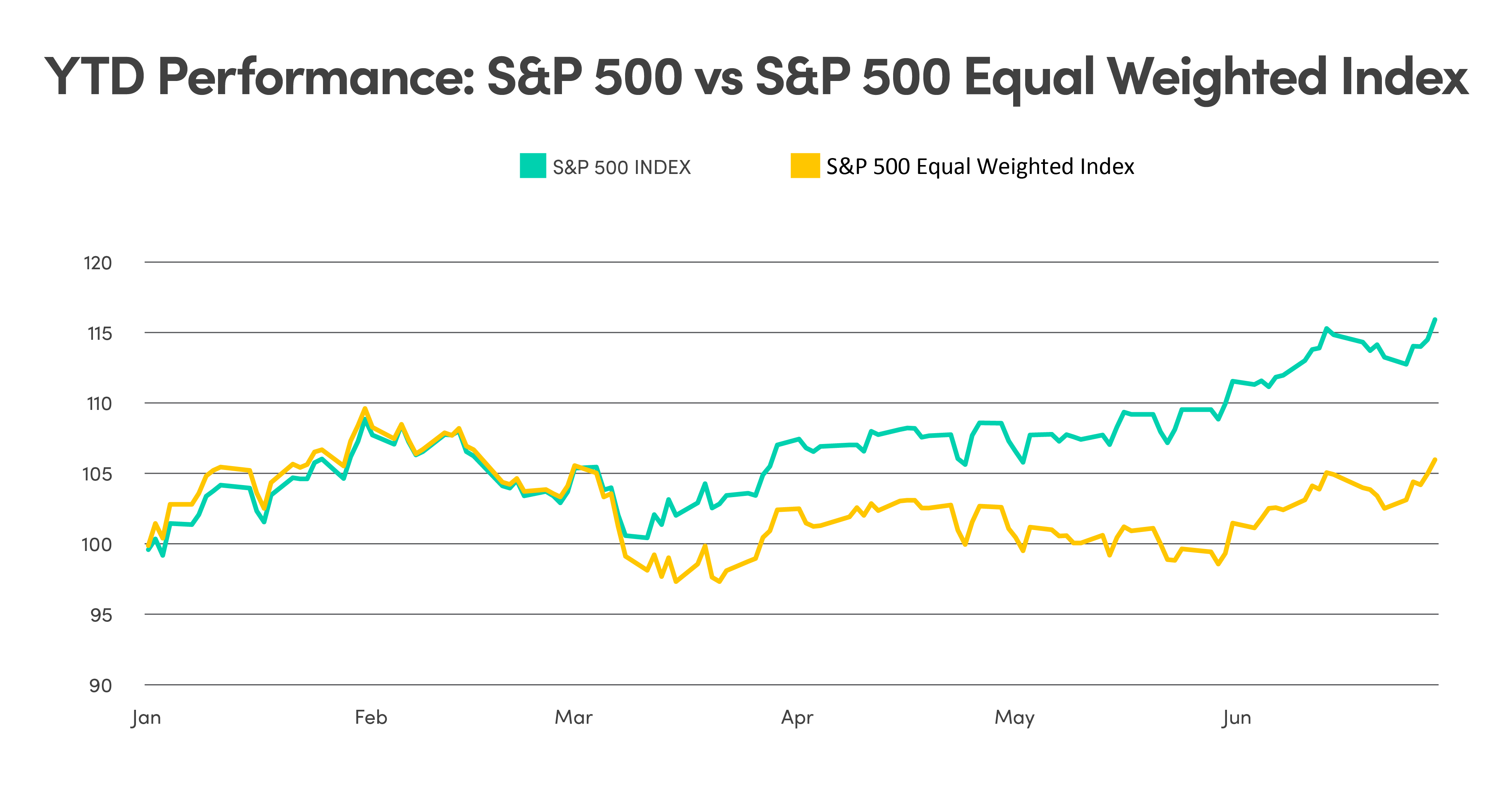

U.S market starting to see improvement in breadth

The S&P 500 Index broke out of its 3800-4200 trading range and entered a technical bull market after returning over 24% since hitting a low in October. While the performance of AI exposed mega-cap technology companies has led the markets, the rally has recently broadened with the equal-weighted index outperforming the market-weighted index in June, pointing to an improvement in breadth and potential for continued upside.

Source: Source: Bloomberg data as of May 31, 2023

As recently as late May, the equal weighted index was flat on a year-to-date (YTD) performance basis.

Source: Bloomberg data as of June 30, 2023

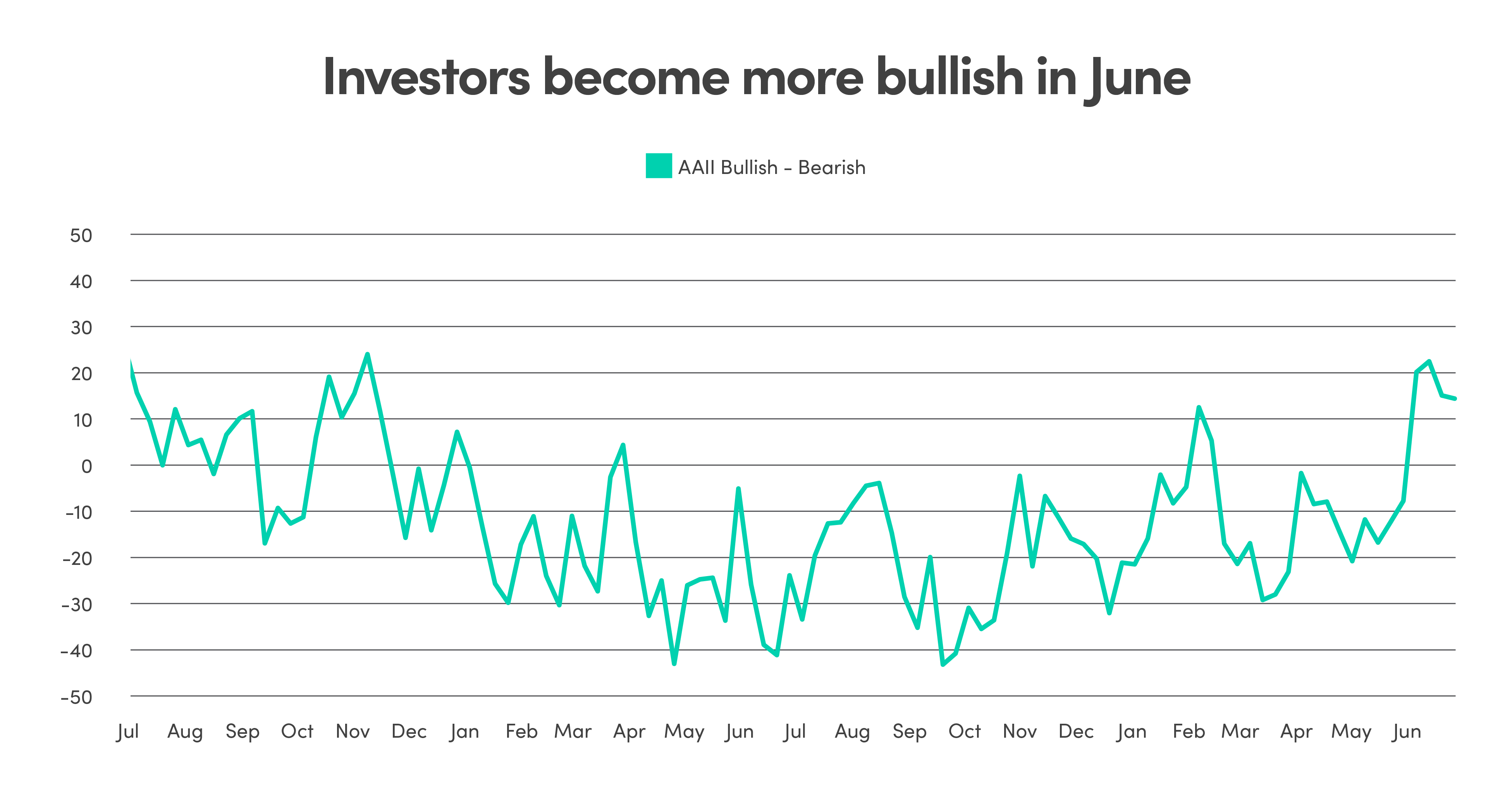

Market strength buoys investment sentiment

Over the course of the past few months, market sentiment has shifted from having more investors in the bearish camp, to having the majority of investors turning bullish. In June, bullish sentiment was at its highest level since November 2021. In other words, this is the most positive investors have been on the markets in almost two years. This can also be seen in investor flows. After several months of outflows, investors moved off of the sidelines and invested into equities in June.

Source: Bloomberg data as of June 30, 2023

Earnings expectations are overly bearish

The market is expecting companies to report a 9% year-over-year decline in the upcoming Q2 earnings season in July, driven by flat sales growth and margin compression. We believe this is a relatively low bar and companies should be able to beat consensus which provides support for equity upside. The key is the companies’ go forward guidance over the next 12 to 18 months in earnings trajectory. Analysts have been consistently revising earnings estimates downward and they may have reached bottom for this year and next year’s estimates. An upward revision in forward earnings estimates would provide the equity markets with a boost in sentiment.