Hot labour market casts doubts on looming recession

The April U.S. employment data released shows that the labour market continues to be strong as with job gains of 253K, bringing the unemployment rate down further to 3.4% from 3.5%, a multi-decade low. There was a moderate uptick in jobless claims as they rose to 242k from 229k. This small increase, along with the drop in the unemployment rate, are not consistent with onset of a recession and will continue to put pressure on inflation over the medium term.

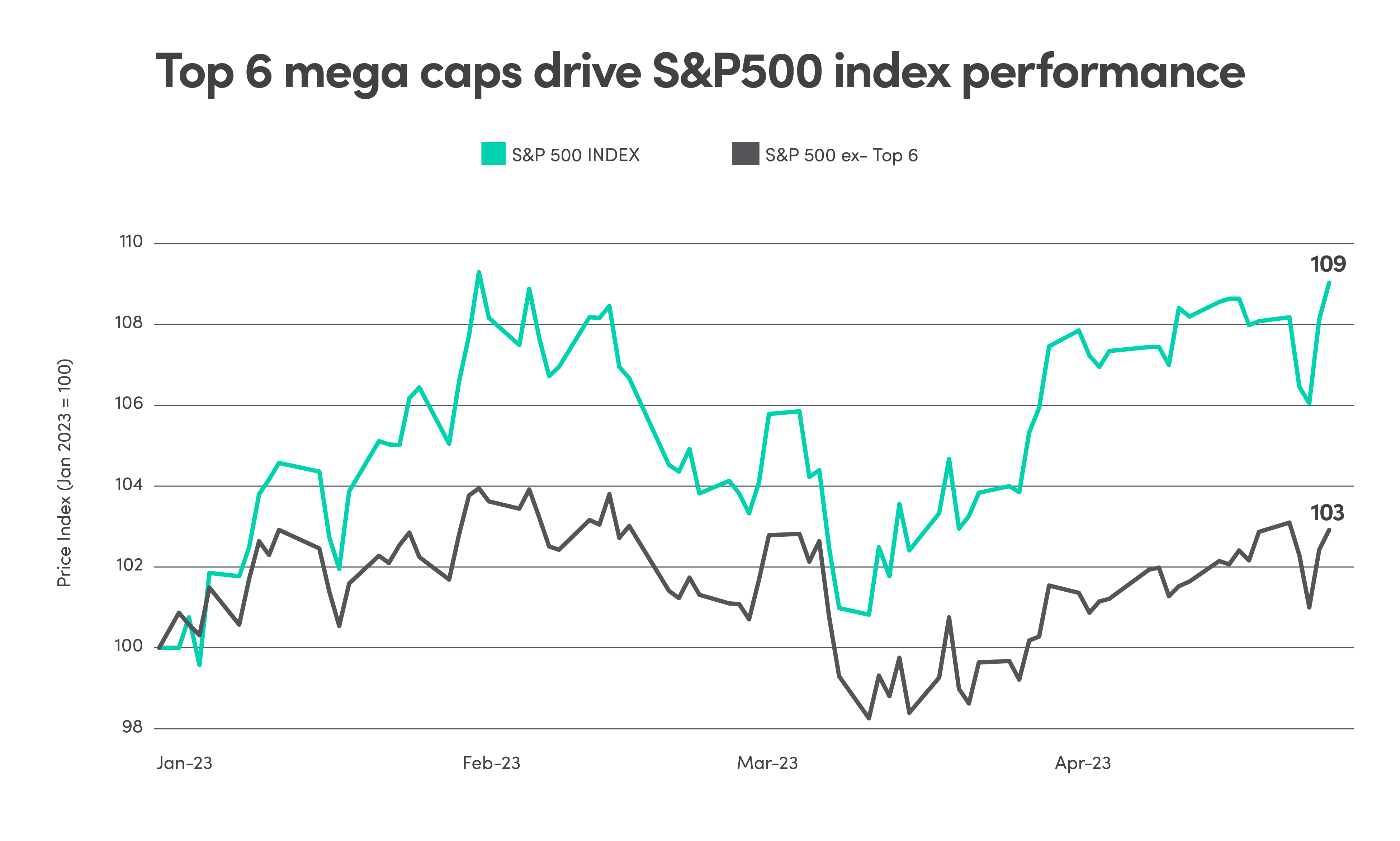

Source: Bloomberg data as of April 30, 2023

However, the effects of the aggressive monetary tightening over the past 12 months could weigh on the economy, cause consumer demand to decline, and cause credit conditions to tighten sometime between late 2023 and early 2024. These could have a significant impact on the markets, even if the economy doesn’t technically fall into a recession by definition.

Large dispersion on earnings growth between sectors

Earning expectations for Q1 2023 were set at a fairly low level following numerous downward revisions based on assumptions of a slowing economy hampered by higher rates, persistent inflation, and tapped out consumers. However, out of the 53% of S&P 500 companies that reported results by the end of April, 78% of them reported positive earnings surprise and 68% reported positive revenue surprise. The actual decline in earnings was 3.3%, versus an estimated decline in earnings of 6.7%.

However, looking at a breakdown of earnings by sector shows lots of dispersion between sectors. Of the 11 sectors in the S&P500, only 4 of them saw earnings growth over the quarter, most notably consumer discretionary, which had earnings growth at 32.6%, (skewed by standouts such as Amazon which beat estimates by 70%). Industrials had earnings growth at 21.2% and Energy had earnings growth at 14.6%. At the other end of the spectrum, materials, utilities, and health care reported negative earnings growth at -25.7%, -20.9% and -15.8% respectively.

The banking sector also proved resilient in the first quarter results despite mounting concerns about the stability of their deposit base. Most of the big U.S. banks, with the exception of Goldman Sachs, posted strong results. Smaller regional banks continue to face headwinds following the collapse of Silicon Valley Bank and Signature Bank of New York. First Republic Bank’s earnings revealed they had over US$100 billion in outflows, resulting in them being taken over by JPMorgan Chase Bank, brokered by the regulators.

Index concentration at record levels

Looking beyond sectors, the year-to-date market rally has mostly been driven by the handful of mega cap companies including Microsoft, Apple, Nvidia, Tesla, Meta, Amazon, and Alphabet. All these mega cap tech names beat estimates in Q1, with Microsoft and Meta having the strongest price performance following earnings. Nvidia had a whopping 90% price return this quarter, closely followed only by Meta at 76%. Alphabet was relatively flat following their beat and Amazon was lower the day after earnings (despite a large but brief gain in after hours) on warnings about AWS’s Q2 revenue.

As mega cap companies continue to lead the rally on the back of strong earnings, they are not only dominating on their year-to-date returns, they also having an outsized impact on the index. The top seven mega cap stocks represent a total of 22% of the S&P 500 and 47% of the Nasdaq Index’s total market cap, they also accounted for 82% of the S&P 500 Index’s year-to-date gains this year. For perspective, the 10 largest stocks in the S&P 500 now make up 26.6% of the total market cap of the index. Apple, the largest company on the S&P 500 Index, has a current market cap of C$3.6T, which is approximately 7% greater than the market cap of the entire Canadian S&P/TSX Composite Index.

As these mega cap companies continue to gain dominance in the cap-weighted S&P500 index, there are increasing concerns about concentration risk along with their rich valuations, as some names continue to climb despite lower growth expectations and falling revenues.

Source: Bloomberg data as of March 31, 2023